The Real Threat to Your Portfolio Isn’t the Market. It’s You.

Most investors believe that the biggest threat to their wealth is a market crash. Headlines reinforce this fear, falling markets, volatile returns, and uncertainty around SIPs often dominate financial conversations.

But the real risk rarely comes from markets.

It comes from life.

Portfolios don’t usually fail during dramatic market downturns they weaken quietly during personal life transitions. These shifts are subtle, often unplanned, and far more disruptive than market volatility.

Let’s understand why.

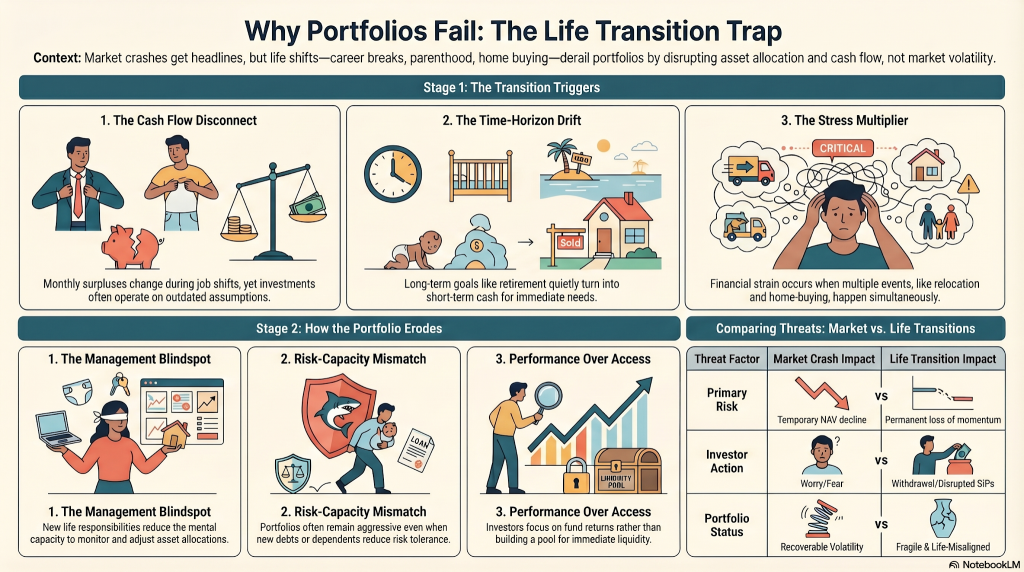

1. Cash Flow Changes Before Your Portfolio Adapts

Most investment plans are built around current income and surplus. But income is rarely constant.

A job change, salary reduction, career break, or relocation can immediately affect monthly cash flow. However, investments SIPs, EMIs, insurance premiums continue as if nothing has changed.Initially, investors try to maintain discipline. But gradually, tighter cash flow forces them to pause or redeem investments. The portfolio doesn’t fail instantly it erodes slowly.

2. Long-Term Investments Quietly Become Short-Term Funds

Investors often assign their money to long-term goals retirement, children’s education, wealth creation.

But life events don’t always follow timelines.

A house purchase, wedding, relocation, or emergency expense creates sudden liquidity needs. Instead of building a separate fund, most investors dip into long-term investments.

Equity meant for 10–15 years gets used in 2–3 years.

This shift in time horizon, often unnoticed is one of the biggest reasons portfolios underperform.

3. Portfolios Are Built for Returns, Not Liquidity

Most investors focus on Returns, Fund selection, Time horizon

But very few plan for access to money.

When an emergency arises, investors withdraw from what is easily available typically equity mutual funds. Not because it’s ideal, but because it’s accessible.

This disrupts compounding and long-term strategy.

A well-designed portfolio should not only grow wealth it should also provide structured liquidity

4. Life Events Don’t Come One at a Time

Financial plans often assume that major expenses will be spaced out.Reality is different.

Life events tend to cluster- Job change, Home purchase, Marriage or childbirth, Family responsibilities

Individually manageable, but together they strain:- Monthly surplus, Savings ability and Investment consistency

The result? SIPs stop, withdrawals increase, and financial discipline weakens.

5. You Have Less Time to Manage Money During Transitions

During stable periods, investors review portfolios, rebalance, and track progress.

But during life transitions time reduces, priorities shift, financial decisions get delayed

The portfolio continues autopilot, exactly when active management is needed the most.

Asset allocation drifts, risks go unchecked, and opportunities are missed.

6. Your Risk Capacity Changes, But Your Portfolio Doesn’t

Risk tolerance isn’t static it evolves with life.

A single professional with no liabilities can take higher equity exposure. But once responsibilities increase: home loan, family, dependents on the ability to absorb risk reduces.

Yet most portfolios remain unchanged.

This mismatch doesn’t immediately show in returns, but it creates, Stress during volatility, Hesitation to invest and poor decision-making

Over time, this emotional discomfort impacts long-term wealth creation.

The Real Insight: Markets Are Predictable, Life Isn’t

Markets fluctuate, that’s expected. But life introduces:

- Uncertainty

- Timing mismatches

- Emotional decisions

And most portfolios are not designed for this reality. Successful investing isn’t just about choosing the right funds. It’s about building a portfolio that can adapt to your life.

Because in the long run, it’s not market crashes that derail wealth, it’s unplanned life transitions handled without a financial strategy.